The Zero Cash Lifestyle. Is the art of having no money ‘available’ on hand. Does that sound weird? I bet it does, and if it does, I’ll enlighten you. Alright..., that wasn’t a typo! You read that correctly. This is the zero-cash lifestyle. So welcome for this is the current lifestyle of yours truly, “the coding ninja”. So let’s dive in.

Before we began

Throughout this post, I’ll be posting receipts to show you I do indeed live this insane lifestyle. This is not for everyone, and I don’t believe everyone should attempt this. Who should attempt this? This is for the risk taker. That person is crazy enough to risk it all, living on the edge every single day… Ok, so let’s be serious, anyone can be a part of this lifestyle. Once I break it all down, we’ll see it’s not all that crazy… Trying this requires the creation of multiple accounts to diversify your money within the same bank account or multiple bank accounts.

Currently, my everyday spending account sits at $2 with the investment bank Fidelity. That is always kept under 5K in total. If it goes over,... It is transferred to another Investment bank usually TD Ameritrade (Fidelity is used for everyday simple transactions/holding... If I require a little more cash, I just liquidate//a short wait time of 2 days so it works out) My spending account is linked to my everyday debit card. I try my best to keep this account less than $5 by design, As you’ll see in the image below.

If your goal is to be POOR BROKE & HUMBLE… Why are persons insinuating.. That I’m pretending to be rich… WHAT?

— Emmanuel Moore (@kodoninja) July 30, 2022

How did that conclusion occur, I’m trying to be what I am #BROKE I have $2 on hand… ? ? ? Wink* lol pic.twitter.com/c621gSd3o8

A common question you may ask is: If that account is sitting at less than $5. How can I buy lunch or anything else I may need for that day? And that is why you’ll always need to have your phone on you. When I need to make a purchase larger than $5. I log onto my banking app on my phone and transfer the amount that’s needed to that spending account.

Additionally, I don’t carry cash, I avoid it like the plague. If for any reason I do need to make a withdrawal, it’s for that exact purpose and that exact amount. Any leftover cash I deposit or get rid of it. This is done by transferring the needed amount to the spending account and withdrawing at an ATM. The remaining amount if any gets re-deposited, or spent on things at the store I may need or want. Like food or household products soap, etc...

The Why

Zero cash is a bit misleading. Thus it’s a bit of a yes, you have no cash (broke). And yes you do have money (still broke). And no you're not broke. Confusing but did you catch it? Cash/Money. When I say cash I’m referring to cash on hand. Direct money you have access to for spending. These are the funds that have been liquidated or have yet to go liquid. For me, this is money I keep in another checking account used for spending. There’s also another checking account for bills. This account is also used for direct deposits. So let’s break down the three accounts you’ll ever use.

Checking Account 1: For spending [Transfer Account]

Checking Account 2: For Bills [Direct-Deposit Account]

Checking Account 3: For Trading/Investing

I currently do have other accounts listed under this bank account with “Fidelity” never exceeding 5k (as stated above). And a business investing/broker adjacent to these accounts (separate login etc// just like with any other business account w/ any bank.. These accounts are locked (frozen) except for one w/ Fidelity). However, we’ll be focusing on the 3 personal accounts listed above. We touched on the account labeled ‘Checking Account 1’ in the earlier paragraphs. This is your spending money for everyday items. This account is typically kept at $5 or less.

Now onto your account labeled bills. This is the most important account you have. Your paychecks, from your career(s)/ job(s) royalties, or any forms of payment will all be deposited into this account. Your bills will be deducted, and or paid from this account. Or that exact amount is transferred to your spending account linked to your debit card so you may make that payment.

A recommended tip for security is that you should not have a debit card linked to this account for this will be a bulk account. Meaning a large sum of money can be found in this account via deposits from your sources of income until it is transferred to your third account for immediate investment. As another note, I have a second card linked to my 3rd account that usually has a zero balance or a few hundred until more money is liquidated. This is the bulk account that has the most but doesn’t. Mainly because it is all liquid.

A method of transport will look something like this:

Money is deposited into your Bill account

Bills are taken out from this account, or transferred to spend to make that transaction.

95% of the remaining money after bills is transferred from your bill account to your investing trading account (account 3)

Money deposited into your trading/investing is immediately used to purchase stock, bonds, crypto, etc. 98% of the money in this account should be liquid.

5% of the remaining money is kept in your bill account until it’s needed for expenses

Money is transferred to your spending account on a needed basis; from your bill account.

At this point, your bill account should be left with exactly what is needed to savvy your bills. Once your bills are extracted for that month or bi-weekly period. Follow the steps for the method of transport to invest the remaining money. Your spending account should be left with as close to $0 as possible. Keep this in mind before you transfer the remaining money from your bill account over to your investment account. Calculate what you’ll need for groceries, fast food, gas (transportation), amazon, etc. Once your money is invested ‘liquid’ you’ll have to wait a few days to liquidate money for what you’ll need or want to buy.

Rinse & Repeat (monthly or bi-weekly or weekly or possibly daily)

We all don’t make the same amount, nor do we have the same amount due in bills and expenses. Thus, this is where your custom calculation is created. Let me also state make sure you're making money. Now, what do I mean by this? After your bills & expenses are deducted this is the money left over... Now if this amount is hardly anything a few things need to change. You can either

Make more money

Get a second full-time or part-time job

Get a higher-paying job

Pick up side gigs

Learn a skill or trade to net you additional income

Software development

App/Web development

Freelance / Remote position

Trade, Invest

Start an online store (reselling, drop-shipping)

Start doing YouTube, Twitch, etc.

Eliminate expenses

Find a cheaper place to live

Get a roommate

Move in with family

Less to no fast food

Cut back on subscriptions

Stop spending or overspending

… If it's something you can live without eliminating it.

For the deposit accounts, I recommend having investment banks such as TD Ameritrade, Fidelity, JP Morgan, E-Trade, Vanguard, and so on. These have been around for some time there reliable and trustworthy. I'll list links to my top five choices below.

Fidelity

TD Ameritrade

Interactive Brokers

E-Trade

Vanguard

To state again these are the only three accounts that matter in the zero cash lifestyle. Is that it? No. Now we know what to do with our cash from our deposits etc. Let’s take a deeper look at what happens to the money in your third account for trading and investing.

If you remembered this is referred to as ‘Money’ Completely liquid money you will not have access to. These are your actual assets, all of your holdings. All of your money is being held in various investment banks and apps. If it can hold and multiply your money you keep it there. Think of liquid as your money is no longer in physical form. It's water, more water can be added and water can be taken away. You can start with a small glass and end up with a few gallons to an entire ocean full. Your money can be larger one day and less another day due to the ever-changing stock markets and your choice of investments.

Diversifying is key thus currently I have quite a few apps and platforms that I use in addition to the big 5 mentioned above. Now before we dive into what you may want to be investing in. Let’s take a look at a few other supporting platforms you may want to try

| | | | |

| Platforms | Account Minimum | Fees | Rating |

| Fidelity | $0 | $0 | 100/100 |

| Vanguard | | | |

| TD Amararade | $0 | $0 | 90/100 |

| E-Trade | $0 | $0 | 90/100 |

| Webull | $0 | $0 | 100/100 |

| Moomoo | $0 | $0 | 80/100 |

| Merrill Edge | $0 | $0 | 90/100 |

| SoFi | $0 | $0 | 90/100 |

| Ally Invest | $0 | $0 | 90/100 |

| J.P. Morgan Self-Directed Investing | $0 | $0 | 85/100 |

| Acorns | $0 | $3 -$5 | 60/100 |

| M1 Finance | $0 | | 95/100 |

| Betterment | $0 | | |

| Robinhood | | | |

| Twine | | | |

The list can go on and on but for the sake of sanity, we’ll stop there. If you’ve found more that’s great be sure to add them to the list. These online brokerage platforms and non-brick-and-mortar firms are great ways to multiply your money. Some offer Robo advisor services like SoFi and Wealthfront, Betterment, Acorns, Fidelity, E-Trade, and so on. Below you’ll find linked images to more options in detail.

Each one of these platforms is all different but offers essentially the same services. Research a bit on all of them. Try them out and see which ones work for you. I have so many of these accounts I’ve lost track. These are what I call supplemental accounts. So I try not to have more than a few hundred to several thousand on these platforms. Your opinion may differ I have friends who have over a hundred thousand on a Robinhood account. It’s all up to you.

My strategy is 3-5 bulk platforms, then have everything else supplemental. See what works for you. Trying several accounts may need the help of additional money so be sure to learn how to make more money. I’ll also note platforms like Acorns, and Worthy for example invest by rounding up to the nearest dollar. They take the rounded-up money and invest it for you.

Now that’s out of the way let’s do some investing in your trading/investing account(s). At this point, you should have a few hundred in this account to get started. If starting. Meaning your account sits below $25,000 you’ll be doing mostly swing trading and investing. To day-trade, this can only happen 3 times a day due to the PDT (pattern day trader rule). That is if you’re in the USA.

The rule of thumb is to implement some buy-and-hold strategies. Buy low exit high on cash and avoid margin if you can. To be safe I recommend buying blue chip stocks like Apple, Tesla, and Amazon in the beginning. These are extremely large companies that will always have a place in the markets. Meaning there’s so much volume, shares, float, and market capital that these stocks will almost always stay fluid and you’ll safely enter and exit trades, break-even is and profit greatly. A lot of these stocks are so large they hardly move so your money will likely remain the same while you collect dividends if that company offers them.

When going into a trade I recommend that you pick one with a lot of volume and shares outstanding, (float). This ensures you can enter and exit trades freely. Pattern trading with the usage of candle stick charting is a great rule of thumb. They provide the most information to see when to enter trades based on various patterns, and signals that can be found on most broker platforms. These patterns can be found throughout the entire stock life span to help determine when you may profit on your return. And revisit previous patterns that may repeat based on past price actions.

I am a swing trader who looks at charting as if I was day trading to get a proper grasp on the stock patterns and action. A good practice will be to try day trading to get acclimated to candle sticks (3 times daily: 1 entry, 1 exit, and 1 other entry) until your account reaches 25k as I did when the PDR applied.

I’ll go into more detail in another article as all of these cannot be contained in this one article. Below I'll list a few of the many areas to invest and trade your money. You can research further and find more information on kodoninja.com. But for now, let’s take a look at one of these.

Stocks

Bonds

ETF’s

Crypto

NFT’s

Commodities

Hedge Funds

Stocks - If you're a slightly impatient investor like me, stocks will be your best friend. A pro and a con to stock trading are that they move fast. One moment they're up, one moment they're down. For day trades, this is the greatest benefit of trading stocks. Going heavy on a trade of a few hundred to a few thousand shares on a stock trading at $13 or $5 on a .20 cent increase can net you a profit over a few hundred to a few thousand depending on how much you entered the trade with.

I’m a big proponent of swing trading going into trades and exiting a day to a few days later to profit. Again, depending on how much I entered the trade determines the amount of profit netted on that trade.

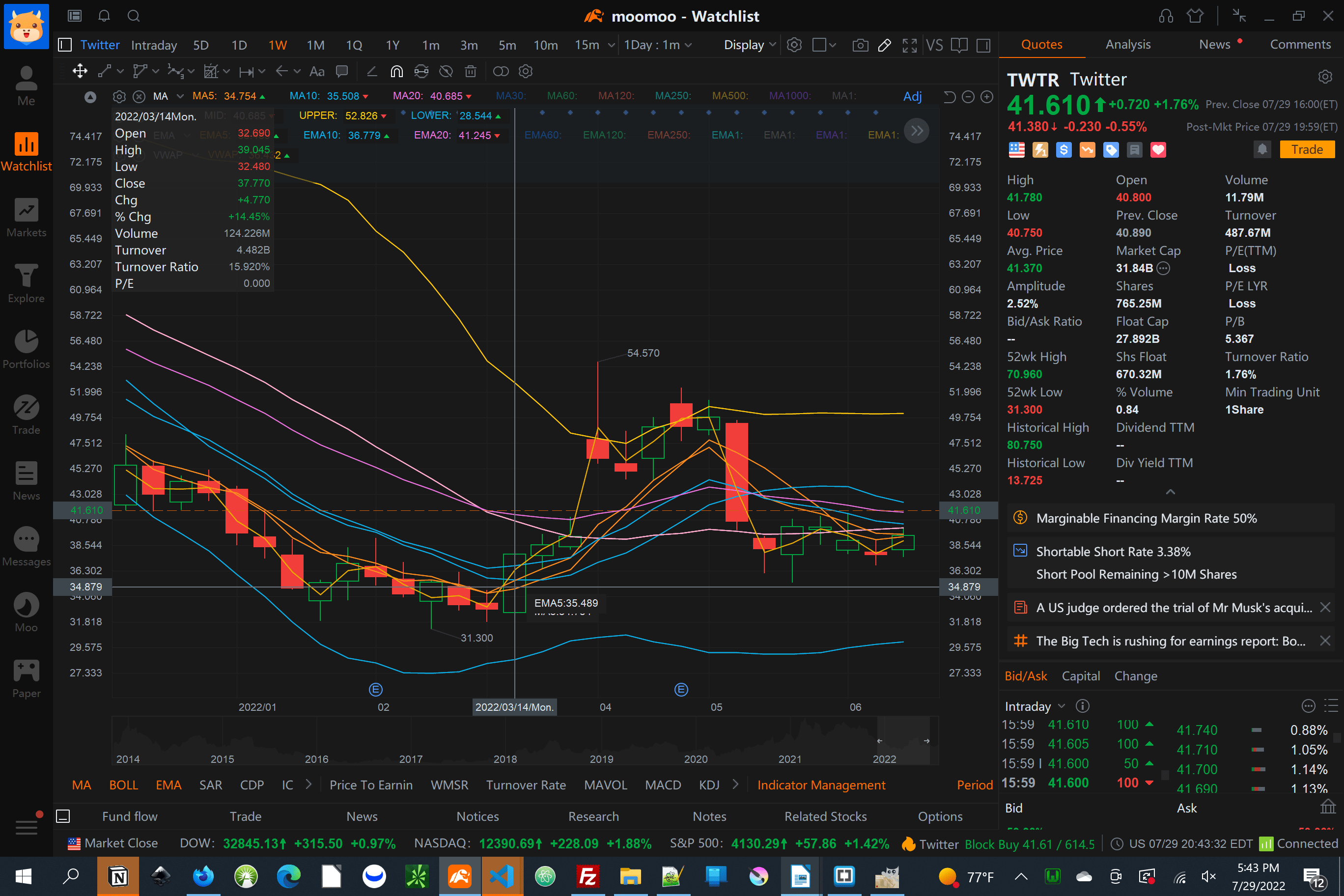

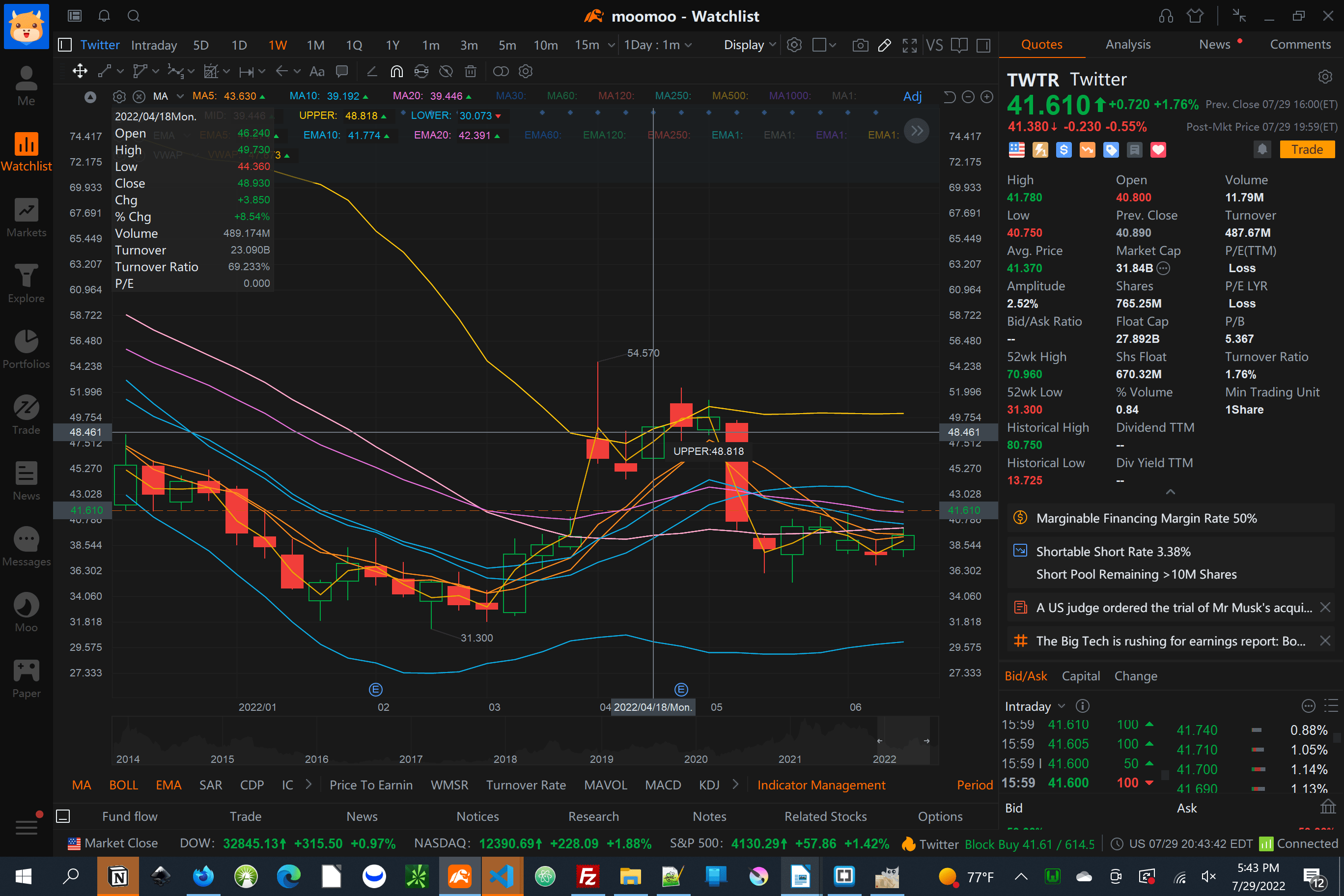

Example of a monthly swing trade from Moomoo

Let’s say we went into the trade with $2,000 worth of shares let’s see how much money we made from that single trade.

We entered the trade on: 3/14/2022 $34.879 (57 shares came out to $1,988.103)

We exited the trade on: 4/18/2022 $48.461 (57 shares came out to $2,762.277)

($2,762.277 - $1,988.103) = $774.147

With our $1,988.103 investment in Twitter stock trading at $34.9, we made $774.15, once we exited the trade at $48.5. This is an example but not something that’ll happen regularly. The stock increased by $13. It may not seem like much, but when you're going into a trade with a few thousand, it packs a punch. A jump like this is gold to any type of trader. If you’re lucky you may find trades that jump like this one within a day or two. Those are the trends I’m looking for. But making nearly $800 in a month on a single swing trade is pretty good. But not nearly as good as making that type of return a day on a single trade.

As you can see swing trading is very lucrative. However, to make this much notice quite a bit of money needs to be tied up to make some serious profit. $2K is a lot of money to be gambling with. The trade may not go the way you want, and you may be stuck in that trade for days to weeks, to just break even… In this example, this trade took over a month. If an emergency happens getting that money out may result in a loss of money. It’s very possible to make these types of gains in a day or week. It all depends on the price movement and volume propelling it. A .70 cent increase on a $5,000 investment on a penny stock trading at .20 cents can more than double your money.

I like the risk vs reward ratio. Swing trading for me has been extremely profitable and has helped to grow my money quite a bit. Since I’m living the zero cash lifestyle. This money doesn’t count. This goes for my everyday banking to my various investment accounts developed over the years. My rule of thumb is once the money is invested it cannot and shall not be liquidated. (except Fidelity) If I have $2 in my spending account and $80 in the billing account that’s what I have to my name as far as I see it. Thus, you’ll have no money until it’s liquidated and transferred for your availability.

PRO’s

Your money can be compounded on interest, gaining quarterly/yearly dividends. Any investments can be sold for profit and reinvested for instance the $774.15 made from that monthly swing trade can be used to go into another well-researched trade. How you choose to do it and the amount is completely up to you. Regardless of the trade, you are building on that overall account value.

Compounded interest gets complex to click the image below to learn more about the link posting

1 year compounded: $5,000 × (1 + (.02 / 1)1×1 = $5,010

<a href=”https://www.bankrate.com/banking/what-is-compound-interest/”><img></a>

The difference in share price increased by 13.6 ($48.461 - $34.879 = $13.582)

Linked below in the example image is a pretty good stock trading calculator I’ve come to love. So far they seem pretty accurate. Thus this is my go-to website.

Conclusion

Regardless diversify your money as much as possible. Invest in a bit of everything, and keep throwing money into the market regardless of if we’re in a bull or bear market. Add to your investment portfolio(s) every other week or whenever you have available cash. I also get life happens; Investing weekly, bi-weekly, or monthly may not be feasible for everyone.

Since you aren’t touching these accounts, there compounding, gaining interest, collecting dividends, and so on. Touching back on life, you may have emergencies that require the need for money. Since your two cash accounts have their purposes. They are always running on E. Thus, you’ll feel the urge to liquidate your assets. If it’s life-threatening, prohibits you from getting to work, health concern, family emergency, or anything extreme goes for it… Just try to rebuild those accounts when applicable. Building a rainy-day fund may also be beneficial however I have rainy investment accounts. I don’t believe in keeping large amounts in banks. For your losing money on inflation and missing out on crypto spikes, stock fluctuations, and higher yield return through various other methods available. Keeping your money liquid puts you in an otherwise gaining position.

We (you and I) keep our money invested because it is useless keeping money in ordinary bank accounts. Inflation and god-awful interest rates. If you had 60k sitting in your checking account it’ll be roughly the same 20 years later. It’ll be worth less with inflation. You lose money by keeping it in banks. All banks are going to do is take your money and invest it for their gain while only returning interest on your initial amount mostly never exceeding 0.01%. All profits made from investing your money are their gain, and you never reap the rewards. Some CDs offer higher interest, and ROI, but on the caveat that you only have access to that account a few times a year. 401k Roth IRA, Seth IRA, and so on can be good options they can be used as assets for investment properties. There is no penalty for investing in a rental property or investing in those accounts just as you would your investment accounts.

A cool thing about some 401k’s is that if your job matches what you put in. That’s less initial money needed for investing. They’d often double your input. You can invest and trade the matched 401k, reinvesting those profits. Then take that money for a down payment to invest in rental properties or property of your own (15/30-year fixed loan) if you see fit. Implement the BRRR (Buy, Rehab, Rent, Refinance, Repeat) method, then that’s another sick cash flow income stream.

I’ll end it here, for there are limitless avenues to invest and reinvest your money. Check out my article “My guide to become a Billionaire Pt.1”. For many other investment ideas while you undergo the zero-cash lifestyle.